Page 134 - P3951_HA_AR14-15_Final Full Set_Chi_20160111_4pm

P. 134

Independent Auditor’s Report and Audited Financial Statements

獨立核數師報告及經審查的財務報表

Notes to the Financial Statements 財務報表附註

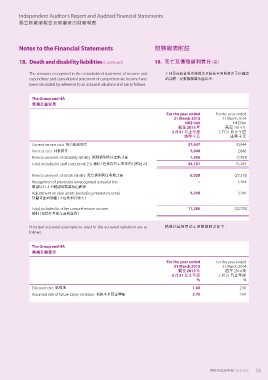

18. Death and disability liabilities (Continued) 18. (續)

The amounts recognised in the consolidated statement of income and 下列是在綜合收支結算表及綜合全面收益表予以確認

expenditure and consolidated statement of comprehensive income have 的款額,是根據精算估值得出:

been calculated by reference to an actuarial valuation and are as follows:

The Group and HA

Current service cost 現行服務開支 For the year ended For the year ended

Interest cost 利息開支 31 March 2015 31 March 2014

Remeasurement of disability liability 傷殘福利責任重新計量 HK$’000 HK$’000

Total, included in staff costs [note 23] 總計(包括在員工成本內)[ 附註 23] 2015 截至 2014 年

Remeasurement of death liability 死亡福利責任重新計量 3 31 3 月 31 日止年度

Recognition of previously unrecognised actuarial loss 港幣千元

確認以往未予確認的精算估值虧損 27,447 30,844

Adjustment on plan assets (excluding interest income) 5,048 2,848

計劃資產的調整(不包括利息收入) 1,606 (2,403)

31,289

Total, included in other comprehensive income 34,101

總計(包括在其他全面收益內) (27,315)

6,028 1,304

Principal actuarial assumptions used in the actuarial valuation are as –

follows: 3,286

5,258

The Group and HA (22,725)

11,286

精算估值採用的主要精算假設如下:

Discount rate 貼現率 For the year ended For the year ended

Assumed rate of future salary increases 假設未來薪金增幅 31 March 2015 31 March 2014

2015 截至 2014 年

3 31 3 月 31 日止年度

% %

1.60 2.50

3.70 3.60

2014-2015 131